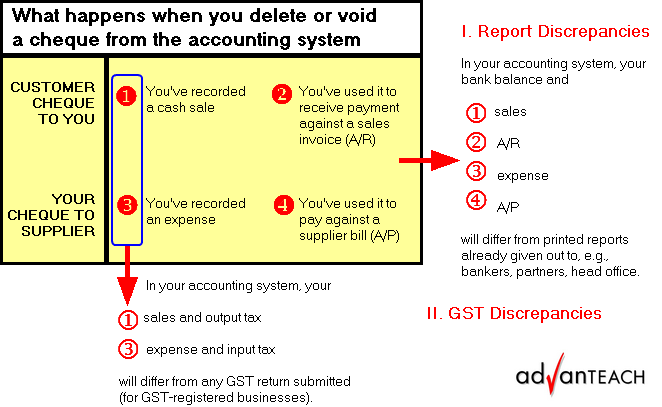

Bank reconciliation is easy to understand Does it feel good to receive a returned cheque from the bank? Never. As a business owner, it means that my work is not paid, and maybe even cheated. Five years ago, I had to bank in three cheques from a customer for the same invoice because the first two cheques bounced. In fact, the third cheque had to be presented to the bank twice before it cleared. Today, I can tell you the exact cheque numbers and dates of the whole sequence of events. Do I need a photographic memory to do that? Not at all. Let me explain the traditional method you should use to keep an electronic trail within your accounting software. Before that, you should think thrice before deleting a dishonoured cheque. In some software, you can easily delete/void a cheque received or paid. You may be tempted to do that for a dishonoured cheque. But you should not. Why? 1. To retain an electronic trail. 2. Secondly, to keep your published financial reports consistent with your accounts, you should not delete a bounced cheque, however immaterial the amount. Deleting a cheque changes your accounts retrospectively - refer diagram below - and requires that you amend distributed reports.  Assuming an accrual basis of accounting 3. Lastly, you should not delete a cheque that has already shown up in your bank statement and, because of month-end cut-off, will only appear as bounced and reversed in the next month's bank statement. (Your accountant might have matched the cheque against the bank statement and prepared a bank reconciliation report. Deleting such a reconciled cheque creates a mismatch in your next bank reconciliation). With these constraints in mind, the logical option is to do the following:

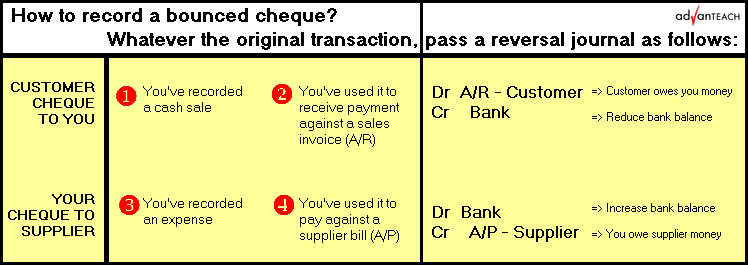

Do not delete a bounced, lost, or damaged cheque. Instead, reverse. For QuickBooks users, read more on How to Handle a Bounced, Spoiled, or Lost Cheque at QCOM's website here. Comments are closed.

|

AddBellsUsingSmartEffects

WriterKenny Goh

Categories

All

© Copyright 2011-2017

All rights reserved |

© 2022 advanteach.com | All rights reserved | Contact: xunwen at advanteach dot com